SoFi’s Price Prediction: The Case for Double-Digit Upside

The post SoFi’s Price Prediction: The Case for Double-Digit Upside appeared first on 24/7 Wall St..

SoFi Technologies (NASDAQ:SOFI) has been one of the most punished fintech names of 2026, but our model says the selling has gone too far. Our 24/7 Wall St. price target points to double-digit recovery over the next 12 months, supported by 30% growth, accelerating product innovation, and a CEO who keeps buying stock in the open market.

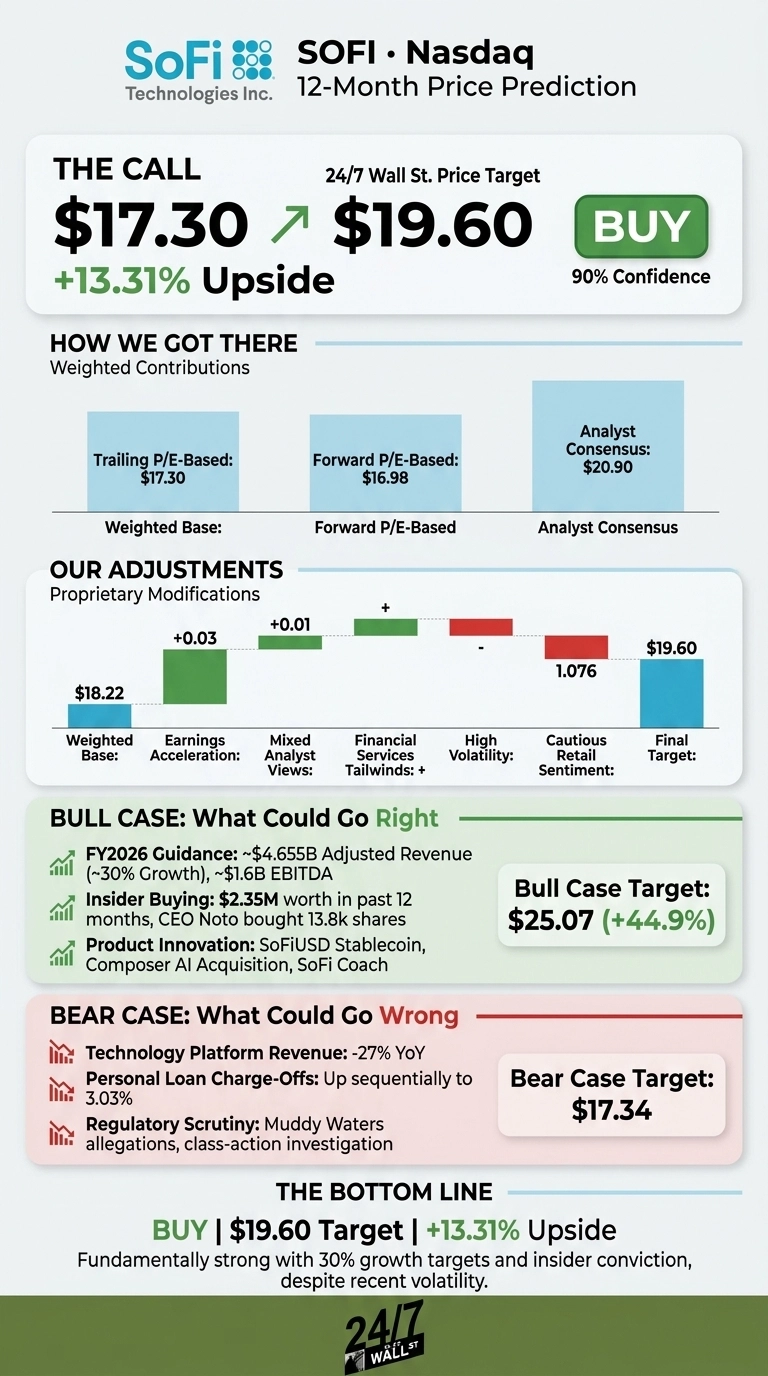

Our 24/7 Wall St. price target for SoFi is $19.60, implying upside of 13.31% from the current $17.30 quote. We rate shares a buy with high confidence (90%).

24/7 Wall St.

24/7 Wall St.

| Metric | Value |

|---|---|

| Current Price | $17.30 |

| 24/7 Wall St. Price Target | $19.60 |

| Upside | 13.31% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Rough 2026, But the Story Is Changing

SoFi has shed 33.92% year to date and sits 36% below its 52-week high of $32.73. Yet the past month tells a different story: shares are up 8.26% as investors digest catalysts.

Q1 2026 results, filed April 29, 2026, delivered revenue of $1.10 billion (topping estimates by 5%) and EPS of $0.12, in line with estimates. Net income jumped 134.45% YoY to $166.73 million, and loan originations hit a record $12.18 billion, up 68% YoY.

Since then, SoFi launched the SoFiUSD stablecoin with a Mastercard settlement partnership, acquired Composer Securities for AI-driven retail trading, and rolled out SoFi Coach.

Why Bulls See a Breakout Ahead

The bull case rests on SoFi’s compounding ecosystem. Management is guiding to FY2026 adjusted revenue of $4.655 billion (~30% growth), adjusted EBITDA of $1.6 billion, and adjusted EPS of $0.60. Medium-term, leadership targets an adjusted EPS CAGR of 38% to 42% through 2028.

Anthony Noto purchased 13,888 shares on June 16 at roughly $18.06, framing the quarter as “We had an excellent Q1 delivering another quarter of durable growth and strong returns.”

Insiders have bought $2.35 million worth of stock over the past 12 months. Add stablecoin optionality, the Composer AI acquisition, and a Rule of 40 score of 72%, and our bull case scenario reaches $25.07, a 44.9% total return.

The Risks Worth Watching

Technology Platform revenue fell 27% YoY on a large client departure, personal loan charge-offs ticked up sequentially to 3.03%, and net interest margin compressed by 63 bps in average asset yields. Short seller Muddy Waters has alleged aggressive accounting, and a class-action investigation is open. Morningstar trimmed its fair value to $17 from $19, and Zacks rates shares a #4 (Sell).

The Tech Platform weakness reflects one lumpy client loss from a single contract rolling off, and credit metrics remain well inside management’s 7% to 8% net cumulative loss assumption. Our bear case scenario sees just $17.34, essentially flat.

SoFi Price Prediction 2026-2030

The 24/7 Wall St. price target sits at $19.60, a buy rating with 90% confidence. The gap between fundamentals (30% growth, 10 straight GAAP-profitable quarters, record originations) and a stock cut by a third year to date makes this compelling.

The thesis hinges on tolerance for the 2.15 beta and exposure to fintech’s most diversified profitable platform. The setup weakens if Muddy Waters’ allegations gain traction or if charge-off rates accelerate beyond management’s loss tolerance band.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $19.60 |

| 2027 | $21.50 |

| 2028 | $23.40 |

| 2029 | $24.90 |

| 2030 | $26.37 |

These projections assume SoFi sustains 30% revenue CAGR and steady margin expansion. Significant upside could come from stablecoin adoption at scale or S&P 500 inclusion. Downside risk centers on credit deterioration or regulatory pressure on the digital asset strategy.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and SoFi Technologies didn’t make the cut. Grab the names FREE today.

The post SoFi’s Price Prediction: The Case for Double-Digit Upside appeared first on 24/7 Wall St..

You May Also Like

SEC And CFTC Seek Public Comment On Portfolio Margining Rules

WTI Falls Below $70.50 as Middle East Oil Supply Surge Reshapes Market Dynamics

Wendy’s Gains 6% Amid “Save Wendy’s” Meme Campaign: Low P/E and Huge Yield Could Make WEN Worth Saving