Down 15% in the Last 12 Months, Can EQT Stock Come Back in 2026?

Key Takeaways:

- Record Free Cash Flow: EQT generated more than $1.8 billion in free cash flow in Q1 2026 alone, roughly matching its entire 2022 output.

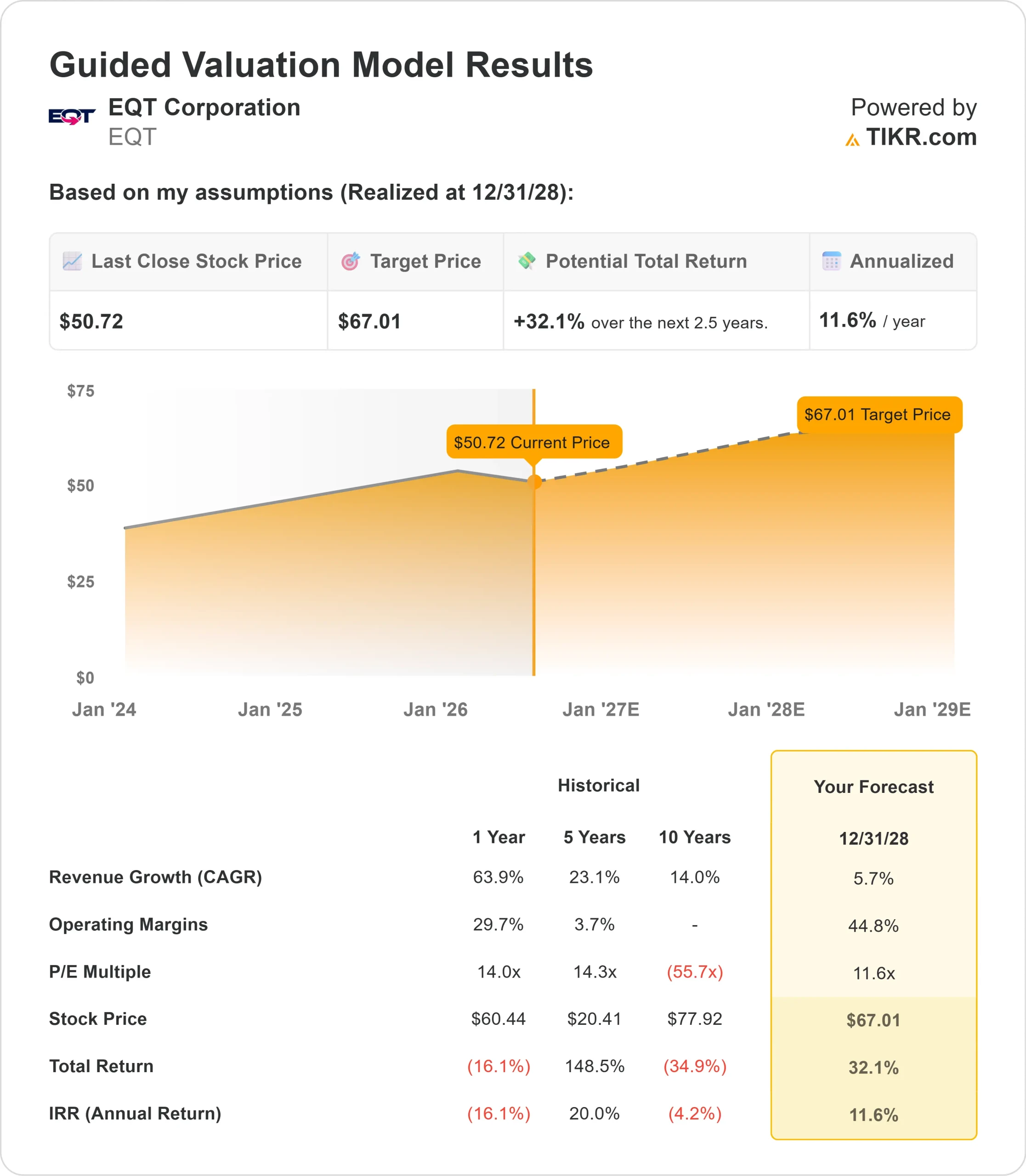

- Price Projection: Based on current execution, EQT stock could reach $67 by December 2028.

- Potential Gains: That target points to a 32% total return from the current price of $50.72.

- Annual Return: Investors could see roughly 12% annual growth over the next 2.5 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

EQT Corporation (EQT) delivered a historic Q1 in 2026. Record free cash flow of $1.8 billion came from a combination of surging natural gas prices, peak winter production, and EQT’s vertical integration through the Equitrans acquisition.

Production came in above the high end of guidance despite Winter Storm Fern.

- Net debt fell to just under $5.7 billion, with leverage below 1x net debt-to-EBITDA.

- Fitch upgraded EQT to BBB during the quarter.

- EQT retired more than $1.7 billion in senior notes in a single quarter.

- If its LNG portfolio were fully operational today, EQT projects 2026 free cash flow would reach approximately $6 billion.

Despite the strong results, EQT trades just above $50, still below year-ago levels. Investors who believe U.S. natural gas demand is entering a structural upturn may see meaningful upside here.

See analysts’ full growth forecasts and estimates for EQT stock (It’s free) >>>

What the Model Says for EQT Stock

We looked at EQT, America’s largest natural gas producer, at an inflection point, at the intersection of three powerful demand drivers: AI data centers, LNG exports, and power generation growth.

EQT’s integrated model is the key differentiator. By controlling the molecule from the well through more than 3,000 miles of midstream infrastructure to end-markets, the company can surge volumes into peak pricing windows.

This is exactly what happened in Q1, with EQT capturing nearly 100% of the winter price surge while peers suffered significantly more downtime during the storm.

Looking ahead, management sees natural gas-fired power demand growing by 6 to 10 Bcf per day, with several multi-gigawatt projects announced in its Appalachian backyard.

Data center and power developers are approaching EQT as a preferred supply partner. LNG contracts beginning in 2030 add another layer, with the potential to generate $500 million in annual free cash flow at current strip prices.

Using 5.7% annual revenue growth and 44.8% operating margins, our model projects the stock reaching $67 within 2.5 years. This assumes an 11.6x price-to-earnings multiple, down from the current forward P/E of 12.6x. The compression reflects normalization as commodity price volatility moderates.

Our Valuation Assumptions

EQT Stock Valuation Model (TIKR)

EQT Stock Valuation Model (TIKR)

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for EQT stock:

1. Revenue Growth: 5.7%

Revenue grew 63.9% over the past year, boosted by high gas prices and the Equitrans integration.

The near-term assumption moderates as prices normalize. The longer-term growth driver is demand.

Management sees its bull case of 10 Bcf per day of new power demand now looking like the base case, with multiple large-scale projects actively in negotiation for gas supply and midstream buildout.

2. Operating margins: 44.8%

EBIT margins averaged 38.2% over the trailing year, a sharp improvement from prior years.

The integrated model and low-cost Appalachian asset base support structurally higher margins than pre-Equitrans levels.

Management highlighted that even after paying more than $1 billion in cash taxes in Q1, free cash flow still exceeded $1.8 billion.

3. Exit P/E Multiple: 11.6x

EQT trades near 12.6x forward earnings today. We assume mild compression to 11.6x.

The stock has traded at 14x over the past year and 16x over three years.

A return to structural demand growth and LNG exposure could push the multiple back toward those levels over time.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Natural gas producers face commodity price cycles and regulatory uncertainty. Here’s how EQT stock might perform under different scenarios through December 2030:

- Low Case: If revenue grows 4.6% a year and net margins settle near 29.5%, investors still see a 32.8% total return (6.4% annually).

- Mid Case: With 5.1% growth and 31.6% margins, the model points to a 64.9% total return (11.6% annually).

- High Case: If data center and LNG demand drives 5.6% growth and margins reach 33.2%, returns could hit 97.7% total (16.2% annually).

EQT Stock Valuation Model (TIKR)

EQT Stock Valuation Model (TIKR)

See what analysts think about EQT stock right now (Free with TIKR) >>>

The range reflects a business where the upside is structural and the downside is commodity-driven.

In the low case, gas prices fall, demand projects take longer than expected to finalize, and the multiple stays compressed.

In the high case, large-scale power and data center projects in Appalachia come online ahead of schedule, LNG offtake agreements accelerate, and EQT captures outsized free cash flow growth through the end of the decade.

How Much Upside Does EQT Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

추천 콘텐츠

GE Vernova (GEV) Stock Surges 5% on Bernstein’s Bullish Initiation

Franklin Templeton Eyes Sept. 1 Launch For Bitcoin Dividend ETFs

Top U.S. economist says Gold reversal is imminent

인기 뉴스

더보기