Uber Stock Rose 6% in a Single Day. Here’s Where the Stock Could Go in 2026

Key Stats for Uber Stock

- Current Price: $73.85

- Target Price (Mid): ~$155

- Street Target: ~$104

- Potential Total Return: ~110%

- Annualized IRR: ~18% / year

- Earnings Reaction: (3.08%) (May 6, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Uber Technologies (UBER) rarely moves 6% in a day. So when shares closed up 6.00% on June 24, 2026, the market was saying something. The catalyst was not a robotaxi headline or a deal rumor. It was a quieter idea bulls have argued for months: Uber Eats is becoming a store, not just a kitchen.

That is the tension. The business keeps compounding, yet the stock spent most of 2026 getting sold, drifting to within a few dollars of its 52-week low of $67.19 before this bounce. Bulls see a platform widening its market with every new retail category. Bears see a name that already prices in a lot and faces an autonomous future that could reshape ride-hailing economics. The question the market still cannot answer: is the retail push a real second growth engine, or a sentiment trade-off on a beaten-down chart?

What happened on June 24

Uber added five retailers to the Uber Eats marketplace: Kiehl’s, FedEx Office, Blick Art Materials, Academy Sports + Outdoors, and Choice Pet. Shoppers can now order skincare, shipping supplies, art materials, sporting goods, and pet products through the Uber Eats, Uber, and Postmates apps. The names join an existing roster that includes Sephora, The Home Depot, and Best Buy.

The market read it as a step change in how Uber Eats is positioned. Shares rose 6.00% to close at $73.85, the best session in about a month, off a base near multi-year lows.

Why does adding five retailers matter? Because it reframes the unit. In the official announcement, Hashim Amin, Uber’s Head of Retail for North America, said “consumers are increasingly turning to Uber Eats for more than meals.” Non-restaurant retail is higher-frequency, and it pulls users toward Uber One, the membership program that gives members a $0 delivery fee on eligible retail orders. More categories mean more reasons to keep the subscription, and subscription revenue is stickier than one-off food orders.

The rally had help. Tigress Financial Partners raised its price target to $115 the same week while keeping a Buy rating, calling Uber a “scaled utility platform.”

Uber Drawdowns (TIKR)

Uber Drawdowns (TIKR)

See historical and forward estimates for Uber stock (It’s free!) >>>

Do the fundamentals support the bounce?

The recent numbers are strong. For fiscal 2025, Uber reported $52.0 billion in revenue, up 18.3%, with Mobility at $29.7 billion and Delivery at $17.2 billion. LTM EBIT margin sits at 11.7%, up from low single digits a few years ago, so the company is expanding margins as it grows.

The retail expansion plugs into Uber’s most underappreciated asset: Delivery. At the Bernstein Strategic Decisions Conference on May 28, 2026, CFO Balaji Krishnamurthy said “our Global Delivery business is quite underappreciated,” citing market-leading positions in Canada, the U.K., France, Australia, Taiwan, and Japan. That reframes Delivery from a margin drag into a durable growth vector, the exact lens the retail news invites.

He also tied retail to membership at the same event. Roughly two-thirds of Delivery gross bookings now come from Uber One, versus only one-third on Mobility, and cross-platform users remain about 20% of the eligible base. That gap is the opportunity: every new retail category gives a Mobility-only user another reason to cross into Delivery and subscribe.

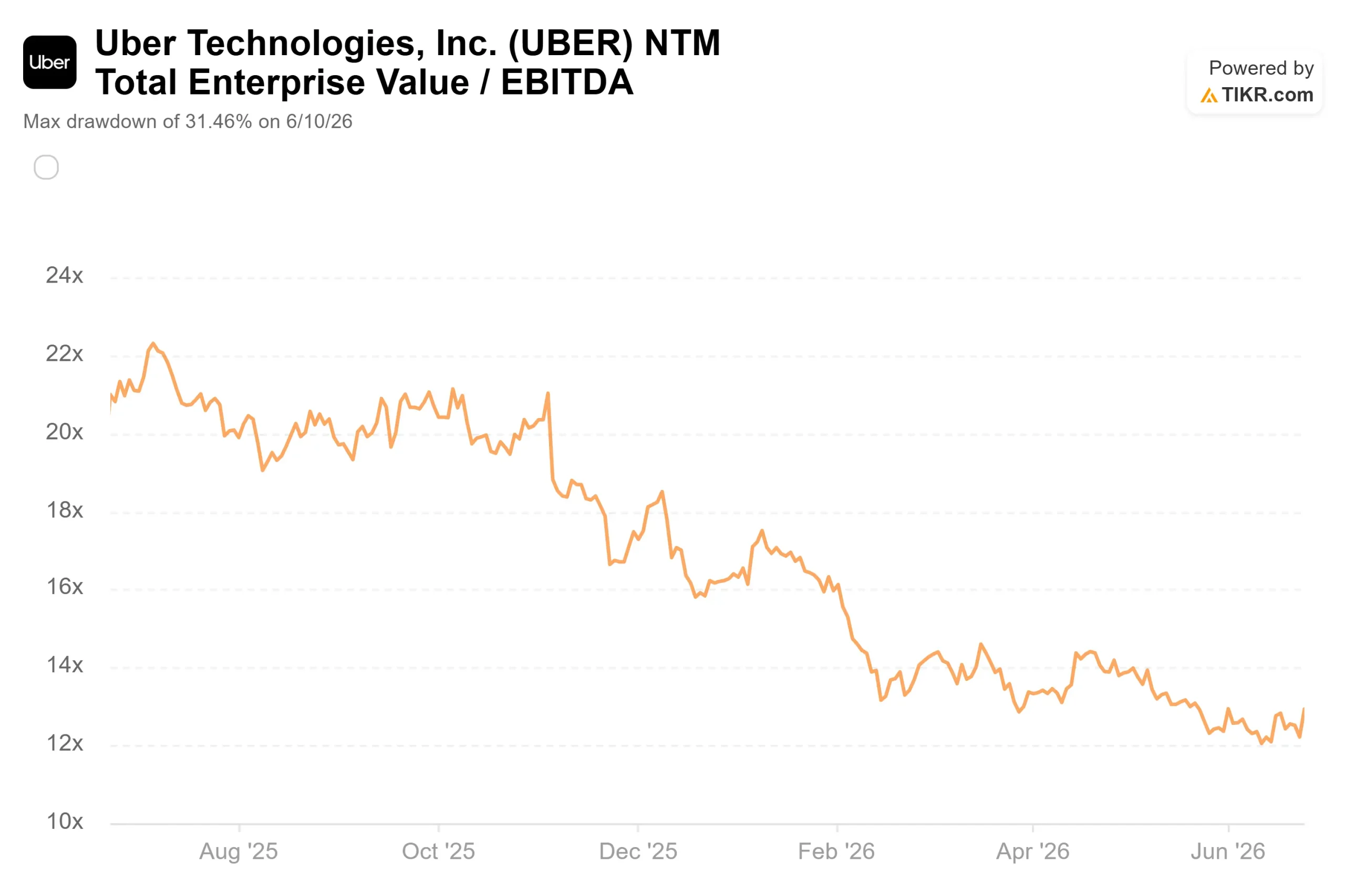

Uber NTM EV/EBITDA (TIKR)

Uber NTM EV/EBITDA (TIKR)

See how Uber performs against its peers in TIKR (It’s free!) >>>

The other side is real. The retail catalyst is incremental, not transformational, and one target raise does not reset a thesis. Uber’s last earnings reaction was negative: shares fell 3.08% on May 6, 2026, despite a beat, as the market focused on estimate compression and the pace of margin expansion. Add an autonomous future that could pressure take rates and the cost of Uber’s AV and M&A ambitions, and caution is coherent. The move shows sentiment is fragile enough to swing hard on good news. It does not prove the re-rating is durable.

TIKR Advanced Model Analysis

- Current Price: $73.85

- Target Price (Mid): ~$155

- Potential Total Return: ~110%

- Annualized IRR: ~18% / year

Uber Advanced Valuation Model (TIKR)

Uber Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Uber stock (It’s free!) >>>

The model uses the mid-case scenario, realized at 12/31/30, because it reflects management’s growth-with-discipline framework without layering on optimism. It points to a target around $155, about 110% upside from the current price and roughly 18% annualized.

Two revenue drivers anchor the case. Mobility benefits from sparse U.S. markets that management says grow at double the rate of dense core markets, with Wait & Save and the new Elite tier widening the funnel at both ends. Delivery benefits from grocery and retail, the exact lever the June 24 news pulls. The margin driver is net income margin expanding toward around 16% in the mid case, up from 10.0% in fiscal 2025, helped by U.S. insurance-cost relief. The primary risk is that AV infrastructure spending front-runs its revenue, compressing margins before monetization catches up.

The upside: if retail and membership deepen the platform while margins expand on schedule, the ~$155 mid case is reachable, and the Street’s ~$104 mean target looks conservative.

The downside: if growth normalizes into the low teens and AV spend drags profitability, the recent multiple compression shows how fast the re-rating can stall.

Conclusion

Watch Q2 gross bookings growth against management’s guided 18% to 22%, due at the next earnings report in early August 2026. A print at or above the high end, with continued margin expansion and visible Uber One growth, confirms the flywheel this move is betting on and makes the bounce look like the start of a re-rating. A miss, or signs that AV and M&A spending is denting margins, hands the bears their proof. Until early August, Uber is a compounding platform priced like a single-product stock, and the retail push is the first concrete test of whether that gap closes.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Uber?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Uber, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Uber alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Uber on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Alabama Enacts Dual Legislative Breakthrough in Blockchain and Judicial Reform

Digital Currency X Technology Enters Into Securities Purchase Agreement for a Private Placement of US$700 Million of Units, Payable in U.S. Dollars or Digital Assets, to Advance Its Digital Asset Treasury Strategy

Jeers rain down on Sean Duffy over Great American Fair remarks: 'You're garbage'