Intel vs TSM: Which Chip Giant is the Better Investment?

The post Intel vs TSM: Which Chip Giant is the Better Investment? appeared first on 24/7 Wall St..

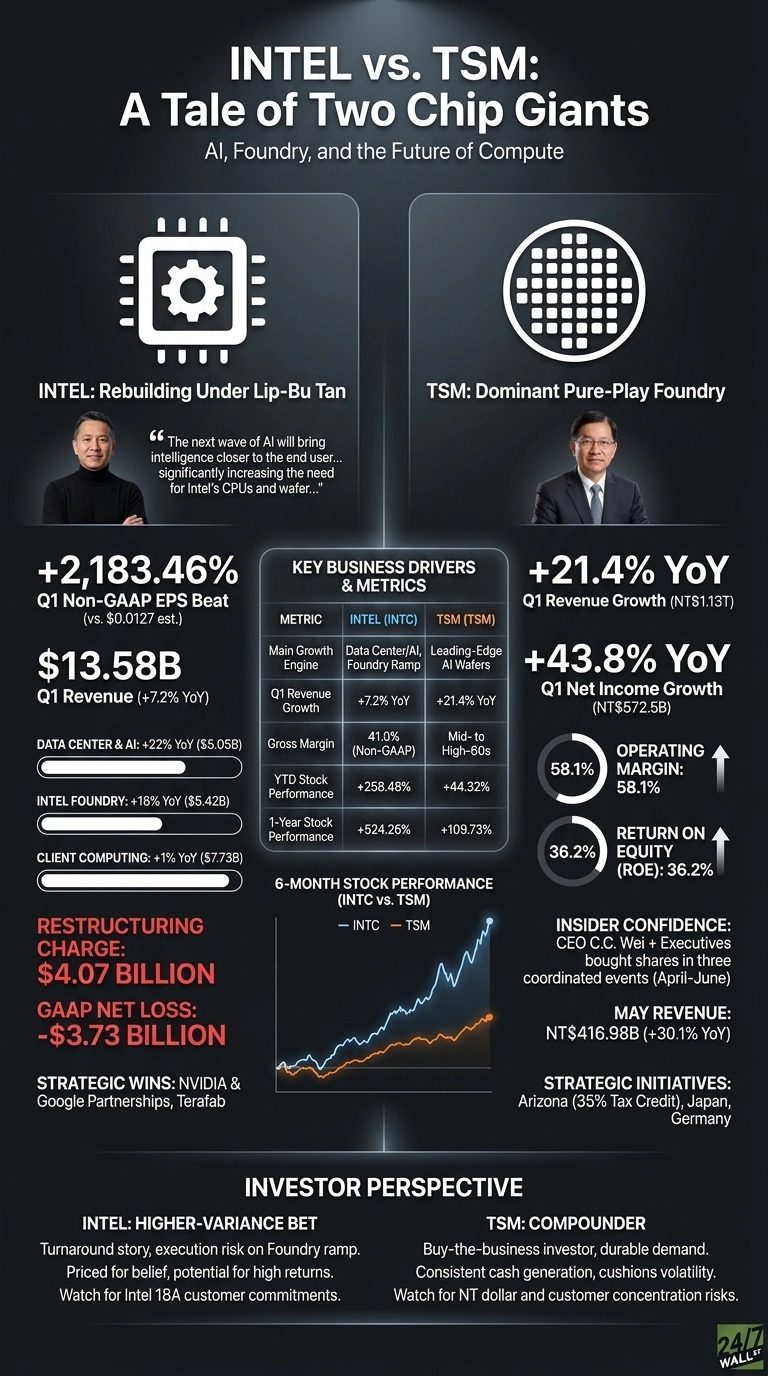

Intel (NASDAQ:INTC) and Taiwan Semiconductor Manufacturing (NYSE:TSM) just delivered very different earnings stories. Intel posted a 2,183.46% non-GAAP EPS beat under CEO Lip-Bu Tan while absorbing a $4.07 billion restructuring charge.

TSMC kept compounding, with Q1 revenue rising 21.4% YoY and net income jumping 43.8%. Both sit at the heart of the AI hardware buildout, on very different footing.

AI Servers Lift Intel. Leading-Edge Nodes Lift TSMC.

Intel’s Data Center and AI segment grew 22% YoY to $5.05 billion, and Intel Foundry climbed 16% to $5.42 billion. Client Computing, the legacy PC business, barely moved at 1%. That mix tells you where the energy is.

Lip-Bu Tan framed it bluntly: “The next wave of AI will bring intelligence closer to the end user, moving from foundational models to inference to agentic.” Strategic wins back the talk: Xeon 6 was selected as the host CPU for NVIDIA’s DGX Rubin NVL8 systems, and Google signed on for custom ASIC IPUs.

TSMC is operating on a different plane. May revenue alone hit NT$416.98 billion, up 30.1% YoY, and management is guiding to over 30% full-year revenue growth. The 58.1% operating margin reflects pricing power on advanced nodes that no one else can match at scale.

24/7 Wall St.

24/7 Wall St.

| Business Driver | Intel | TSMC |

| Main Growth Engine | Data Center and AI, Foundry ramp | Leading-edge AI wafers |

| Q1 Revenue Growth | +7.2% YoY | +21.4% YoY |

| Gross Margin | 41.0% non-GAAP | Mid- to high-60s |

Rebuilder vs. Compounder

Intel is rebuilding a foundry from inside an integrated company. The $5 billion NVIDIA equity stake, the Google ASIC deal, and the Terafab tie-up with SpaceX, xAI, and Tesla all point to one bet: that U.S. leading-edge capacity has strategic value buyers will pay for.

The hitch is execution. Intel Foundry is still losing money, and management has flagged a potential pause of Intel 14A if customers do not commit.

TSMC’s path is simpler. Stay the only credible volume supplier of leading-edge nodes, then collect rent. Its Arizona expansion is now eligible for a 35% investment tax credit effective January 1, 2026, which softens the geopolitical hedge cost.

On insider activity, TSMC saw three coordinated buy events between April and June with CEO C.C. Wei adding shares each time, while Intel’s CFO and foundry GM were net sellers in May and June.

The Next Test Is Foundry Conversion

For Intel, Q2 guidance of $13.8 billion to $14.8 billion in revenue at a 39% gross margin suggests momentum without margin breakout yet. I will watch whether Intel 18A volume in Arizona converts external customers into multiyear wafer commitments.

For TSMC, the question is whether NT dollar appreciation and customer concentration (top 10 customers = 84% of receivables) start to bite reported growth.

TSMC the Compounder, Intel the Higher-Variance Bet

Intel has run hard. The stock is up 258.48% year to date and 524.26% over one year, which already prices in a lot of belief. TSMC is up a more measured 44.32% YTD while actually producing the cash flows.

For me, TSMC fits a buy-the-business investor: 46.5% profit margin, 36.2% ROE, and durable demand. Intel suits a turnaround investor willing to underwrite Foundry losses for the chance that Tan’s reset reshapes the cost base. Intel’s risk/reward at current levels skews to execution risk on the Foundry ramp, while TSMC’s cash generation cushions volatility on pullbacks.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Taiwan Semiconductor Manufacturing didn’t make the cut. Grab the names FREE today.

The post Intel vs TSM: Which Chip Giant is the Better Investment? appeared first on 24/7 Wall St..

You May Also Like

AI predicts XRP price for April 30, 2026

Trezor Academy Releases Documentary on Africa’s Bitcoin Economy, Opens Education Donations

Ripple Price Prediction: Will the CLARITY Act Trigger a Repricing Event for XRP?