Employment Data and Monetary Tightening Concerns Threaten Market Stability This Week

Quick Summary

- The S&P 500 has gained over 7% year-to-date in 2026 though June has seen market weakness

- Thursday’s employment report could intensify speculation about potential rate increases

- Federal Reserve officials adopted a more aggressive tone recently, prioritizing inflation management

- Chip stocks rallied 85% from March bottoms before experiencing sharp declines this week

- Consumer price growth exceeded 4% for the first time since 2023, driven by energy sector pressures

Investors enter the coming week facing dual concerns: Thursday’s employment figures and heightened volatility in technology shares. The prospect of monetary tightening combined with erratic chip sector performance has created uncertainty as 2026’s first half concludes.

Year-to-date, the S&P 500 has climbed more than 7%. However, June has proven challenging, with equities surrendering portions of their earlier advances.

E-Mini S&P 500 Sep 26 (ES=F)

E-Mini S&P 500 Sep 26 (ES=F)

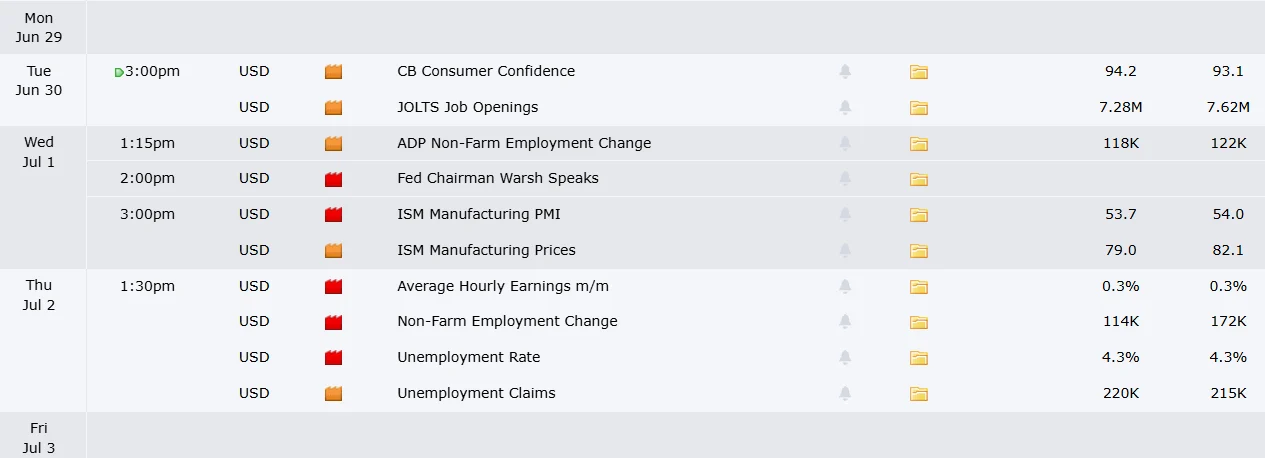

Employment Figures Take Center Stage

The June employment situation report arrives Thursday. Consensus forecasts from Reuters-surveyed economists project approximately 110,000 new positions added last month. May’s data showed 172,000 job gains, marking the third consecutive month of healthy employment expansion.

Source: Forex Factory

Source: Forex Factory

Robust employment growth could trigger negative market reactions. Market participants fear strong data would increase the likelihood of Federal Reserve rate increases rather than reductions.

Fed funds futures currently indicate greater than 50% probability of a rate increase by September. This represents a dramatic shift from early 2026 expectations of rate reductions by year-end.

The Federal Reserve communicated clearly at its most recent policy meeting that inflation containment remains the top priority. Consumer price growth has now surpassed 4% for the first time in three years, partially attributed to elevated energy prices connected to Middle Eastern tensions.

Monetary tightening increases financing costs for both businesses and households. It also dampens economic expansion and can pressure equity valuations downward.

Chip Sector Faces Headwinds

Technology equities have dominated market narratives for months. The Philadelphia Semiconductor Index surged 85% from late-March market lows. Yet the index retreated this week as market participants questioned valuation sustainability.

Micron Technology delivered robust quarterly results Wednesday, providing some sector stability. Nevertheless, the Nasdaq declined over 4% for the week.

Oil prices have moderated, falling to approximately $70 per barrel from $100 monthly ago following Middle Eastern ceasefire developments. Sustained price levels could alleviate inflationary pressures.

Nike’s quarterly earnings release is scheduled for next week. The broader second-quarter reporting season intensifies in mid-July.

The Federal Reserve faces a challenging environment. Employment data surprises in either direction could rapidly alter market expectations as the year’s second half begins.

The post Employment Data and Monetary Tightening Concerns Threaten Market Stability This Week appeared first on Blockonomi.

You May Also Like

Chainlink Whale Activity Rises While Price Bleeds for 7 Straight Months

Binance Invests $300 Million Annually in Compliance, Reports $10.5 Billion in Fraud Blocked