Coca-Cola Stock Trades at $81 With a $86 Analyst Target and $105 TIKR Mid-Case: The Gap Explained

Key Takeaways for Coca-Cola Stock as of July 2026

- Analysts rate Coca-Cola stock 12 buys, 7 outperforms, 5 holds, and 1 underperform, with a mean price target of $86, implying 6% upside from the current price of $81.

- TIKR’s mid-case model values Coca-Cola at $105 by December 2030, implying 30% total return, or 6% annualized.

- Coca-Cola posted 3% unit case volume growth and 10% organic revenue growth in Q1 2026, sustaining 20 consecutive quarters of overall value share gains, while guiding for 8% to 9% comparable EPS growth for the full year.

See Coca-Cola’s full earnings history and forward EPS estimates on TIKR. Track every analyst revision and target change on KO for free →

Coca-Cola Stock Beats Q1 EPS by 6% While Volume Grows Across All Segments

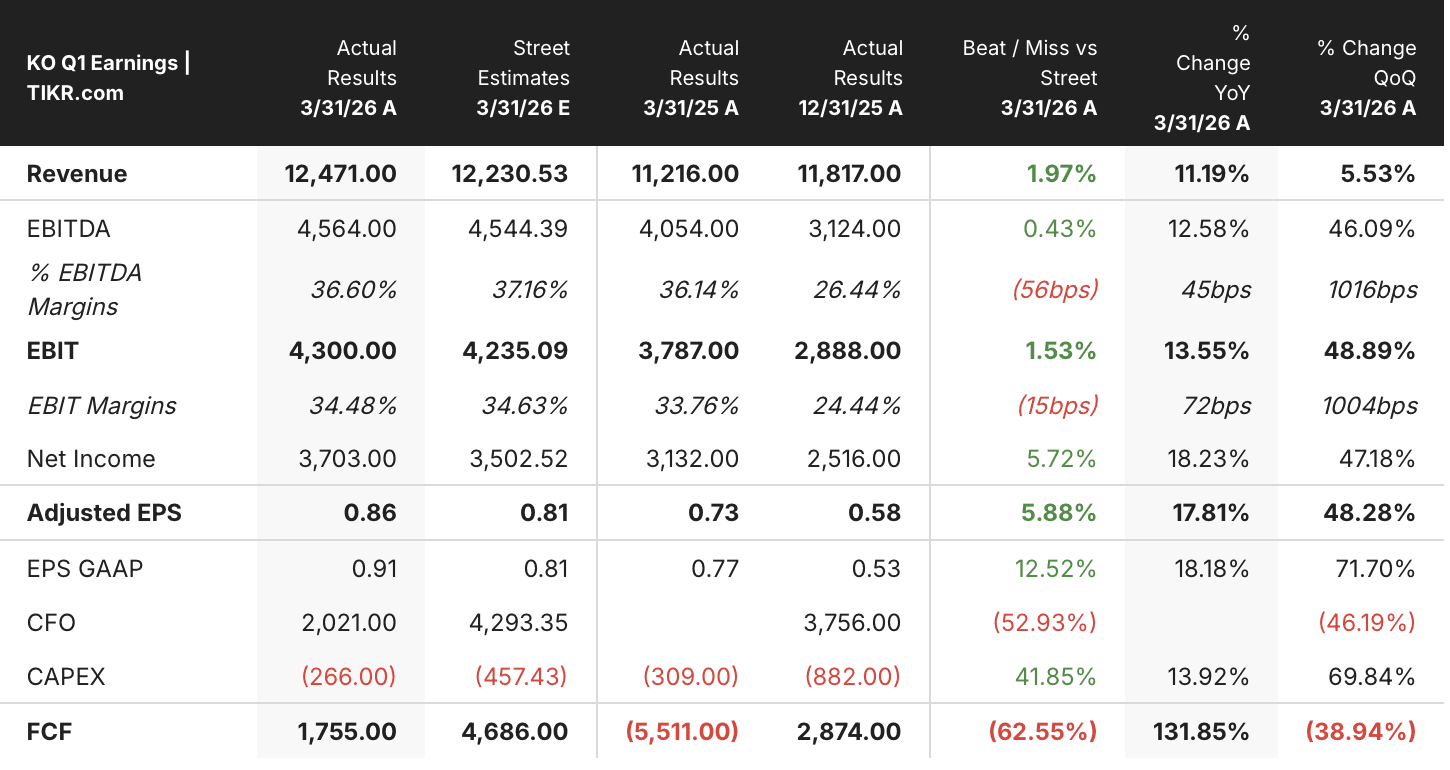

The Coca-Cola Company (KO), the world’s largest non-alcoholic beverage company, delivered adjusted EPS of $0.86 in Q1 2026, a 6% beat above the Street’s $0.81 estimate and an 18% increase year over year.

KO Stock Q1 2026 Earnings in USD (TIKR)

KO Stock Q1 2026 Earnings in USD (TIKR)

Revenue of $12.47 billion beat consensus by 2%, growing 11% from the prior year period, while unit case volume expanded 3% across all six operating segments.

That growth came despite a genuinely complex operating backdrop. CFO John Murphy, presenting at the Deutsche Bank Global Consumer Conference on June 4, addressed the uneven demand environment directly: “The narrative on the consumer being resilient is a nuanced narrative because they’re not all the same. We have segments of our consumer base around the world that are under pressure, and we have a choice to stay relevant with them or not.” His remarks flagged particular strain on consumers earning between $50,000 and $60,000 annually, a cohort where cumulative cost pressures have eroded purchasing power.

What management is doing about it is the structural thesis. Coca-Cola is deploying its revenue growth management architecture across markets, expanding pack-size options from smaller single-serve entry points to premium multi-serve formats, holding value relevance on both ends of the income curve simultaneously.

Beneath the headline numbers, the mix picture showed selective pressure. Price/mix grew 2% in Q1, below recent trend, driven by Easter timing and category mix in North America, stronger value-tier growth in Asia Pacific, and geographic mix effects in Latin America from Mexico’s new sugar tax.

Comparable gross margin contracted approximately 30 basis points, primarily from commodity pressures in tea and coffee. Comparable operating margin, however, expanded 70 basis points as operating expense efficiencies more than offset the gross margin compression.

The bigger story is guidance. Management raised full-year comparable EPS growth guidance to 8% to 9% versus the prior 7% to 8% estimate, aided by a 1-point reduction in the projected effective tax rate to 19.9%. Organic revenue growth guidance of 4% to 5% remained intact. The pending sale of Coca-Cola Beverages Africa, expected to close in the second half of 2026, will mechanically lift overall company margins by removing a lower-margin bottling business from the consolidated results.

Still, geopolitical uncertainty is real. Murphy flagged that the Middle East conflict drove a volume decline in the Eurasia and Middle East segment in March, and that its resolution timeline “is going to be a topic on all of our agenda as we go into 2027.”

See how KO’s Q1 beat compares to prior quarters and what analysts revised after results on TIKR for free →

Wall Street Rates Coca-Cola Stock 19 Buys or Outperforms, With a Mean Target of $86

Street Analysts Target for KO Stock (TIKR)

Street Analysts Target for KO Stock (TIKR)

As of June 30, 2026, 24 analysts cover Coca-Cola stock with 12 buys, 7 outperforms, 5 holds, and 1 underperform.

The mean price target of $86 implies 6% upside from the June 30 close of $81. The high target of $92 and low target of $71 reflect the spread between those who see geopolitical and consumer demand risk as transient and those who view the Middle East disruption as a structural 2027 headwind on mix and pricing power.

Wall Street Expects Coca-Cola Stock’s Adjusted EPS to Grow 7% Through Q2 2027

KO Stock EPS Actuals & Estimates (TIKR)

KO Stock EPS Actuals & Estimates (TIKR)

Coca-Cola delivered adjusted EPS of $0.86 in Q1 2026, beating the Street’s $0.81 estimate by 6% and growing 18% from the $0.73 reported in Q1 2025.

The consensus now models Q2 2026 adjusted EPS at $0.93, a 7% increase year over year, followed by $0.88 in Q3 2026 and $0.60 in Q4 2026. The Q4 figure reflects the known 6-day calendar shift that removes days from the final quarter of the year, a dynamic management explicitly flagged.

The open question is whether the geopolitical overhang in the Middle East and the softness in the $50,000 to $60,000 consumer segment will hold volume growth below the 3% Q1 pace in coming quarters, or whether the FIFA World Cup activation cycle and the fairlife capacity ramp in North America provide enough offset.

TIKR’s $105 Target on KO Stock Holds If EPS Momentum Outpaces the Geopolitical Discount

TIKR’s mid-case model values Coca-Cola at $105 by December 2030, implying 30% total return from the current price of $81, or 6% annualized over 4.5 years.

KO Stock Valuation Model Results (TIKR)

KO Stock Valuation Model Results (TIKR)

For a defensive consumer staples franchise with 20 consecutive quarters of value share gains and a 62-year dividend growth streak, a 6% annualized return places Coca-Cola at the upper edge of what the category typically offers, with meaningfully lower volatility than most equity alternatives.

The path to that target runs directly through the dynamics management named: full-year EPS growth of 8% to 9%, CCBA divestiture margin lift in the back half, and sustained organic revenue growth of 4% to 5%, all of which are already embedded in Q1’s results and management’s updated guidance.

Wall Street’s best ideas don’t stay hidden for long. Catch analyst upgrades, earnings beats, and revenue surprises on thousands of stocks the moment they happen with TIKR for free →

Should You Invest in The Coca-Cola Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The Coca-Cola Company stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Coca-Cola Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze KO stock on TIKR for Free →

Ayrıca Şunları da Beğenebilirsiniz

Why Is ETH Still Weak While Ethereum Staking Hits Record Highs?

Binance Surpasses $1B in Stock Trading AUM within 30 Days