Price Prediction: Nvidia Falls Below $5 Trillion, This is Where It’ll End The Year

The post Price Prediction: Nvidia Falls Below $5 Trillion, This is Where It’ll End The Year appeared first on 24/7 Wall St..

NVIDIA’s (NASDAQ:NVDA) market cap slipped beneath the $5 trillion mark this month, and the stock has given back roughly a tenth of its value in 30 days. After a parabolic spring, the AI bellwether is taking a breath. Our model reads that breath as a buying opportunity.

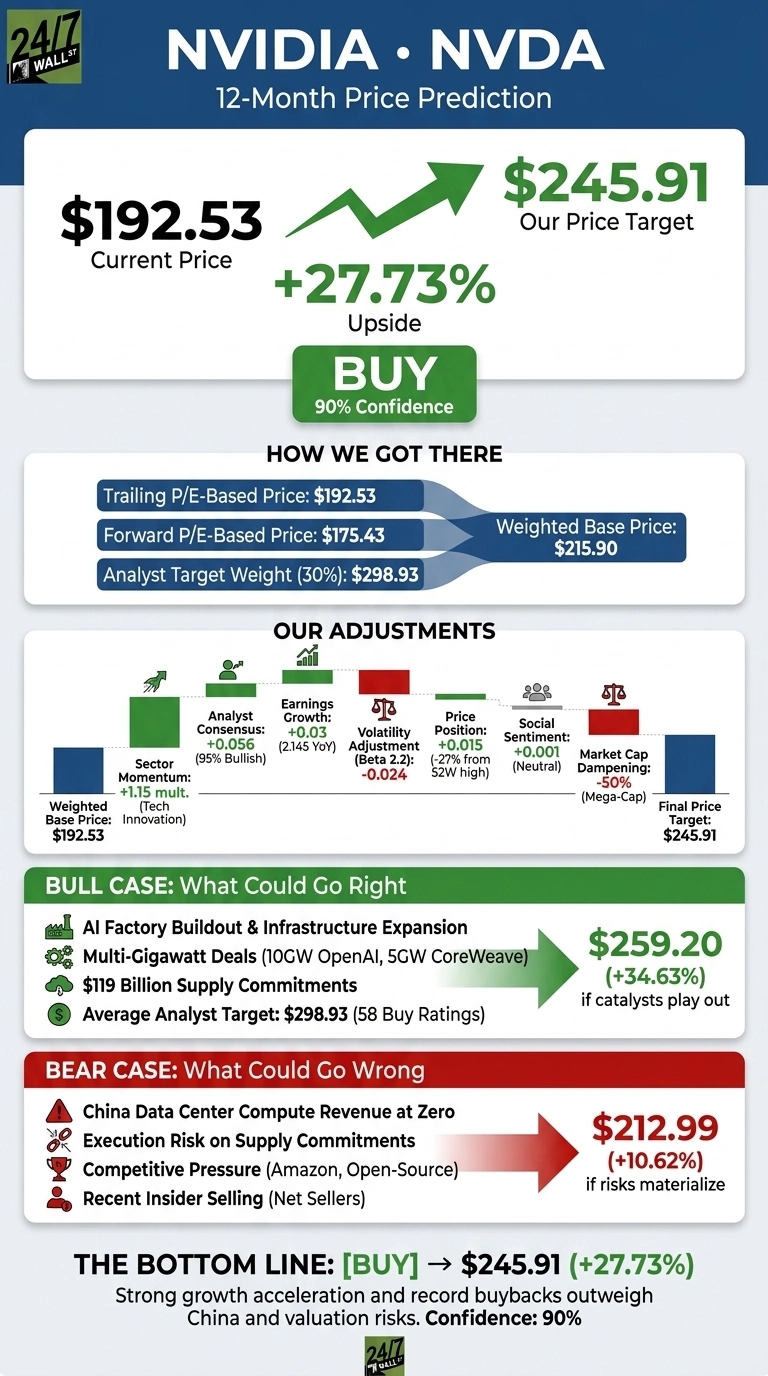

NVDA stock trades at $192.53, with a market cap of $4.663 trillion. Our 24/7 Wall St. price target for NVIDIA is $245.91, implying 27.73% upside over the next 12 months. The recommendation is buy, with confidence at 90%.

24/7 Wall St.

24/7 Wall St.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $192.53 |

| 24/7 Wall St. Price Target | $245.91 |

| Upside | 27.73% |

| Recommendation | BUY |

| Confidence Level | 90% |

The $5 Trillion Pullback in Context

NVIDIA is down 8.62% over the past week and 9.34% over the past month, yet sits up 3.36% year to date and 24.36% over the past year. Shares are roughly 27% off the $236.26 52-week high, with a 52-week low of $151.29. The recent rotation stems from the SK Hynix HBM slowdown narrative and broader AI-chip profit-taking, while NVIDIA’s fundamentals remain intact.

The Q1 FY27 report on May 20, 2026 showed revenue of $81.61 billion, up 85.23% year over year, with non-GAAP EPS of $1.87 beating consensus by 5.42%. Data Center revenue hit $75.25 billion (+92% YoY), networking grew 199%, and Q2 guidance came in at $91 billion. Management approved an $80 billion buyback and lifted the quarterly dividend to $0.25.

The Case for $260 and Beyond

If demand outpaces supply, the bull case takes NVDA to $259.20 by June 2027, a 34.63% return. CEO Jensen Huang describes the AI factory buildout as the largest infrastructure expansion in human history, with partners committing to multi-gigawatt deployments including 10GW with OpenAI, 1GW with Anthropic, and 5GW with CoreWeave by 2030.

Total supply commitments sit at $119 billion, signaling management sees the order book firming. The average sell-side target is $298.93, with 58 Buy ratings against 2 Holds and 1 Sell.

What Could Go Wrong

The bear case takes NVDA to $212.99 over 12 months, still a positive 10.62% return. Risks include China Data Center compute revenue now assumed at zero in guidance, execution risk on the $119 billion supply commitment if hyperscaler capex slows, and competitive pressure from Amazon Trainium and open-source models trained on Huawei silicon.

Insiders have been net sellers across 9 recent transactions. Those sales are routine 10b5-1 dispositions while the company authorized an $80 billion buyback, a stronger institutional signal.

Why the Dip Looks Attractive

The 24/7 Wall St. price target of $245.91 reflects 27.73% upside with 90% confidence and a buy rating. The combination of 85% revenue growth and forward guidance implying acceleration into Q2 tips the scale.

The setup favors investors who can tolerate a beta of 2.2 and the China overhang. The thesis weakens for those who believe hyperscaler capex peaks in 2026, as the multiple has little margin for that disappointment.

Here is where our model projects NVIDIA could trade, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $216.81 |

| 2027 | $262.00 |

| 2028 | $305.00 |

| 2029 | $348.00 |

| 2030 | $391.74 |

These projections assume NVIDIA executes on its Blackwell and Vera Rubin roadmap. Restored China access could drive significant upside, while a reset in hyperscaler spending would compress multiples.

Don't wait: the analyst who called NVIDIA in 2010 just revealed his top 10 AI stocks. See the full list FREE now.

The post Price Prediction: Nvidia Falls Below $5 Trillion, This is Where It’ll End The Year appeared first on 24/7 Wall St..

Ayrıca Şunları da Beğenebilirsiniz

Marvell Stock Rose 7% After UBS Backed a $340 Target on CXL. Here’s Where the Stock Could Go

Hamster Kombat Daily Cipher 2 July 2026: Play And Win