AMD Stock Price Prediction: Strong Analyst Consensus Lifts the Target

The post AMD Stock Price Prediction: Strong Analyst Consensus Lifts the Target appeared first on 24/7 Wall St..

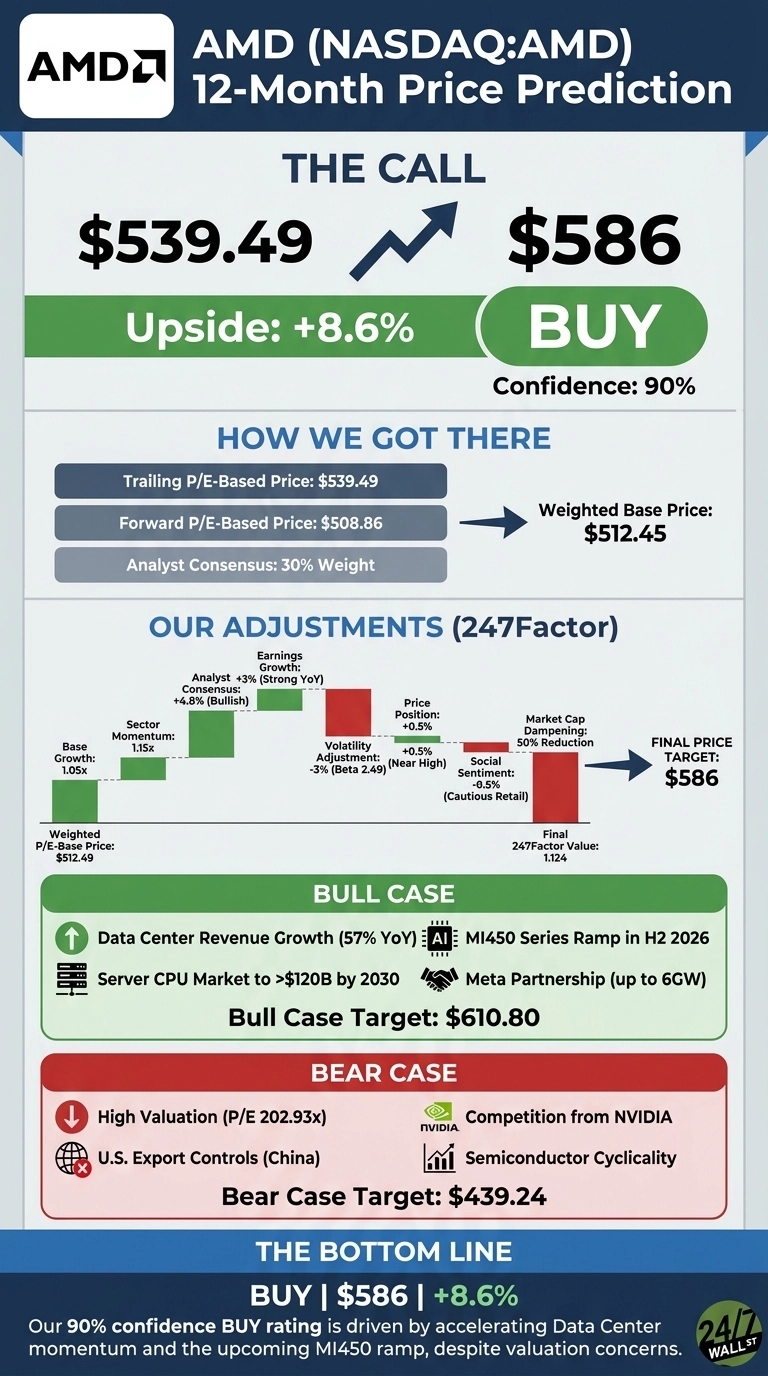

Our Advanced Micro Devices (NASDAQ:AMD) call is straightforward: the 24/7 Wall St. price target for AMD is $586, modestly above today’s price of $539.49. That implies roughly 8.6% upside over the next 12 months, and our recommendation is buy.

Confidence is high at 90%, supported by 80% bullish analyst consensus, an accelerating Data Center business, and the MI450 ramp landing in the second half of 2026.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $539.49 |

| 24/7 Wall St. Price Target | $586 |

| Upside | 8.6% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Vertical Move Since Q1 Earnings

AMD has been one of the year’s defining AI trades. Shares are up 151.91% year to date and 275.14% over the past year, with a 51.86% surge since the May 5 earnings report. The stock sits roughly 11% below its 52-week high of $562.99, well off the $133.50 52-week low.

Q1 FY2026 was the catalyst. Revenue hit $10.25 billion, up 37.85% year over year, with non-GAAP EPS of $1.37 beating estimates by 5.88%. Data Center revenue alone reached $5.78 billion, up 57%. Management then guided Q2 to roughly $11.2 billion, implying about 46% growth.

24/7 Wall St.

24/7 Wall St.

Why Bulls See a Breakout Past $650

The bull case is anchored in TAM expansion. Lisa Su told investors the server CPU market is now expected to grow at “greater than 35% annually, reaching over $120 billion by 2030”, driven by agentic AI workloads that need both CPUs and accelerators.

Customer engagement on MI450 and Helios is “exceeding our initial expectations”, with the Meta deal alone covering up to 6 gigawatts of Instinct GPU deployment.

Cantor Fitzgerald just lifted its target to $700 and UBS moved to $670 on June 29, both citing server CPU share gains. If MI450 ramps cleanly and Data Center AI hits Su’s “tens of billions of dollars” 2027 mark, a bull case to $610.80 within 12 months looks conservative, with $700 reachable on a strong execution quarter.

The Risks Worth Watching

The bear case starts with valuation. AMD trades at a P/E of 203x trailing and an implied 118x on forward EPS, leaving little room for execution slippage.

China remains a wildcard after FY2025 absorbed $440M in net MI308 inventory charges from U.S. export controls. NVIDIA (NASDAQ:NVDA) still dominates AI training, and our model’s bear case pegs downside at $439.24, an 18.58% drawdown.

Insider activity is also worth noting, with 93 recent transactions skewed net-selling. That said, bulls would counter that much of this reflects scheduled 10b5-1 plans after a 275% one-year rally, and free cash flow more than tripled to $2.57 billion in Q1, which softens the valuation critique.

AMD Price Prediction 2026-2030

The 24/7 Wall St. price target for AMD is $586, our recommendation is buy, and confidence sits at 90%. The factor tipping the scale is Data Center momentum: 57% segment growth with management guiding server CPU revenue up more than 70% in Q2.

The constructive case strengthens if MI450 production ramps on schedule in H2. The setup weakens if forward EPS estimates start drifting lower or China restrictions widen further.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $586 |

| 2027 | $640 |

| 2028 | $675 |

| 2029 | $700 |

| 2030 | $730 |

These projections assume AMD continues executing on its Instinct roadmap and that Data Center AI revenue scales toward the “tens of billions of dollars” Lisa Su outlined for 2027. Significant upside would come from MI500 traction; meaningful downside would come from a broader AI capex digestion cycle.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and AMD didn’t make the cut. Grab the names FREE today.

The post AMD Stock Price Prediction: Strong Analyst Consensus Lifts the Target appeared first on 24/7 Wall St..

Ayrıca Şunları da Beğenebilirsiniz

Why Is ETH Still Weak While Ethereum Staking Hits Record Highs?

Binance Surpasses $1B in Stock Trading AUM within 30 Days